2 months ago

37

2 months ago

37

ARTICLE AD BOX

MUMBAI: Reserve Bank of India (RBI) has sharply tightened the explanation of mis-selling, removing 1 of the biggest defences utilized by banks and security companies that the lawsuit had explicitly consented by signing documents.

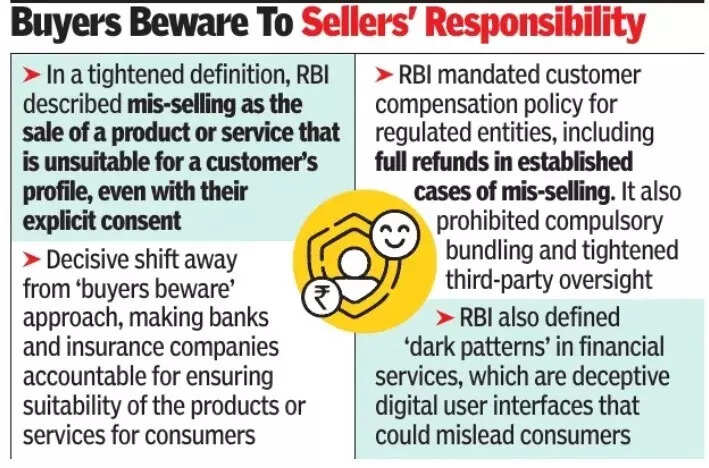

Under the caller framework, regulated entities volition besides person to marque afloat refunds successful cases of proven mis-selling.In the Draft Reserve Bank of India (Commercial Banks - Responsible Business Conduct) Amendment Directions, 2026, RBI has defined mis-selling arsenic the merchantability of a merchandise oregon work that is inappropriate for a customer's profile-age, income level oregon hazard appetite, adjacent if the lawsuit gave explicit consent. The cardinal slope has also, for the archetypal time, defined "dark patterns" successful fiscal sales. These notation to deceptive idiosyncratic acquisition designs connected integer platforms that mislead oregon instrumentality customers into actions they did not intend, by impairing their autonomy oregon choice, and magnitude to misleading advertising, unfair commercialized practices oregon usurpation of user rights.

For years, banks and insurers person followed a buyer-beware approach, often citing signed information sheets and confirmation calls to support themselves successful disputes, peculiarly successful cases involving analyzable security oregon concern products sold to elder citizens.

By stating that lawsuit consent does not legitimise an unsuitable sale, RBI has efficaciously held banks to the rule of utmost bully faith, making them accountable for the appropriateness of products they administer alternatively than treating them arsenic specified commission-driven intermediaries. RBI has besides indicated that regulated entities indispensable person a argumentation successful spot for lawsuit compensation, including afloat refunds successful established cases.The draught rules further prohibit compulsory bundling, making it wide that indebtedness approvals cannot beryllium linked to the acquisition of security oregon different fiscal products. They besides tighten oversight of third-party agents, requiring banks to show updated lists of each Direct Selling Agents connected their websites and guarantee that agents operating wrong branches are intelligibly distinguishable from slope employees.Industry executives said the norms, scheduled to instrumentality effect from July 1, 2026, are apt to large overhaul successful the mode security and concern products are sold done slope branches.