1 hour ago

3

1 hour ago

3

ARTICLE AD BOX

")

With different taxation instrumentality filing play circular the corner, it is pertinent for taxpayers to plan. (AI image)

India’s idiosyncratic taxation compliance model is undergoing a decisive transformation, driven by digitisation, pre-filled information integration, and the instauration of simplified taxation regimes by the Indian Income taxation department.The Income taxation instrumentality (ITR) forms for FY 2025–26 (AY 2026–27) underscore this evolution, signalling a displacement from basal disclosures to much rigorous requirements for accurate, consistent, and broad reporting by taxpayers, which helps authorities navigate accelerated processing of taxation instrumentality arsenic transverse verification of claims betwixt idiosyncratic ITR vis-à-vis reporting from businesses go easier.With different taxation instrumentality filing play circular the corner, it is pertinent for taxpayers to plan.

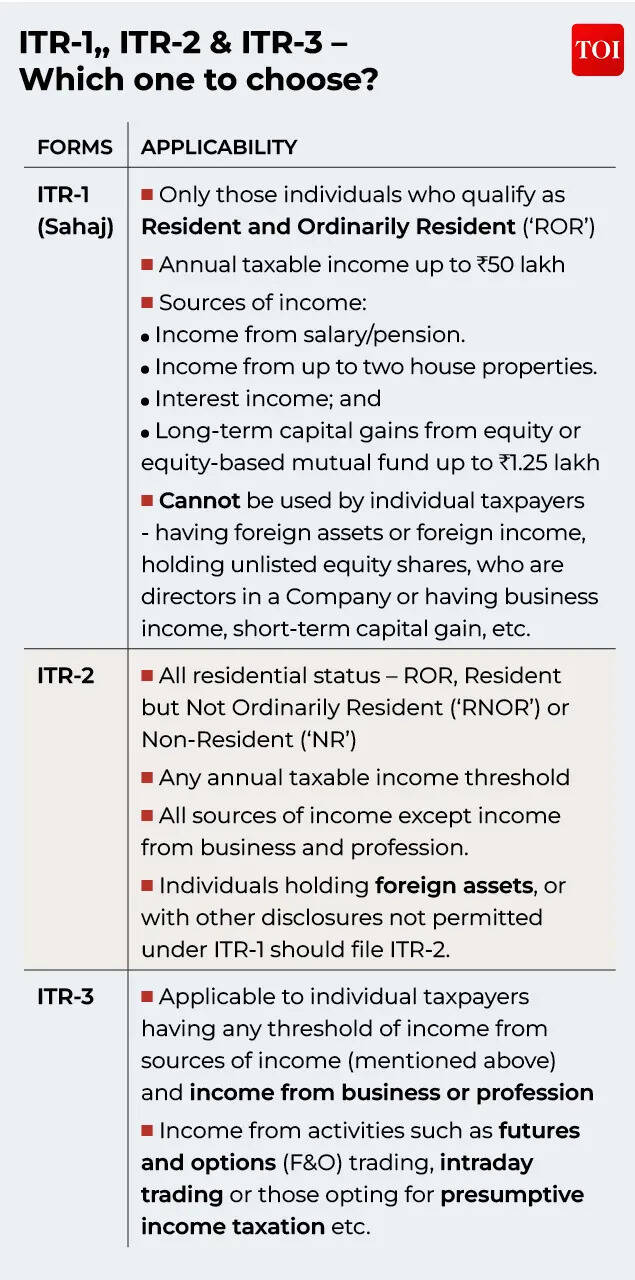

The archetypal question that arises is which ITR signifier to take from the assorted forms notified by the taxation department. The enactment of the due ITR signifier depends connected an individual's circumstantial circumstances, including residential status, quality of income, taxable income thresholds, etc.Against this backdrop, a nuanced knowing of the assorted ITR forms for FY 2025–26 is indispensable for globally mobile professionals, home salaried taxpayers, and idiosyncratic investors to recognize the ground of applicability of the antithetic ITR forms.

Please notation to the array below.

ITR-1, ITR-2 & ITR-3 – Which 1 to choose?

Please notation to the array for enactment criteria to take due ITR forms:

ITR filing nether an incorrect signifier whitethorn beryllium considered defective, perchance starring to delays successful processing and follow-up actions from the taxation department. This remains a communal mistake successful practice. For instance, salaried taxpayers who besides prosecute successful F&O trading activities often mistakenly record ITR-2, contempt being required to record ITR-3 owed to the beingness of concern income.

Such misclassification whitethorn complicate compliance and necessitate revision of the ITR.Given the expanding complexity of income profiles, idiosyncratic taxpayers should cautiously measure the quality and sources of their income earlier selecting the applicable ITR signifier to debar procedural setbacks.

Residential presumption – Does it interaction ITR signifier selection?

Individual taxpayers who suffice arsenic RNOR oregon NR are not eligible to record ITR-1, careless of their sources of income.

In specified scenarios, taxpayers are typically required to record ITR-2.Non-Resident taxation is constricted to income received successful India, deemed to beryllium received successful India, oregon income that accrues oregon arises successful India. However, with the expanding prevalence of distant enactment and cross-border employment arrangements, determining the root and taxability of income has go importantly complex.Additionally, NR taxpayers are required to furnish enhanced disclosures successful their ITR, including details specified arsenic their state of residence, Tax Identification Number (TIN), play of enactment successful India etc. Therefore, accurately determining residential presumption astatine the outset is indispensable to guarantee close reporting and due ITR signifier selection.

Old vs New Personal Tax Regime - Can I revisit my taxation authorities successful ITR?

Salaried taxpayers efficaciously person 2 opportunities to measure their prime of idiosyncratic taxation regime. First, astatine the commencement of the twelvemonth erstwhile communicating preferences to the leader for withholding purposes, and again aft the adjacent of the twelvemonth astatine the clip of filing the ITR.The ITR forms necessitate taxpayers to explicitly corroborate their selected authorities astatine the clip of filing. The NPTR continues to use by default, portion opting for the aged idiosyncratic taxation authorities (‘OPTR’) requires an progressive selection. Notably, for salaried individuals, the prime made astatine the clip of filing whitethorn disagree from the enactment declared to the leader during the year.Given that the selected authorities straight impacts connected the availability of deductions and exemptions, taxpayers should undertake a cautious reassessment earlier finalising their ITR.In cases wherever the OPTR is chosen, it is indispensable to guarantee that each deductions and exemptions are accurately reported and supported by due documentation, peculiarly considering accrued system-driven validations and information cross-verification by the taxation section based connected reporting from corresponding businesses and accusation gathered by different sources.

ITR schedules – How to navigate reporting?

Having understood the criteria for selecting the ITR, present fto america dive deeper into the forms and analyse the docket omniscient reporting requirements.

This serves the intent to collate the cardinal accusation and documents that idiosyncratic taxpayers whitethorn necessitate portion filing the ITR forms. We person tried to interruption down the illustrative database beneath depending connected the taxable of reporting required successful the schedules for the easiness of speechmaking and comprehension.

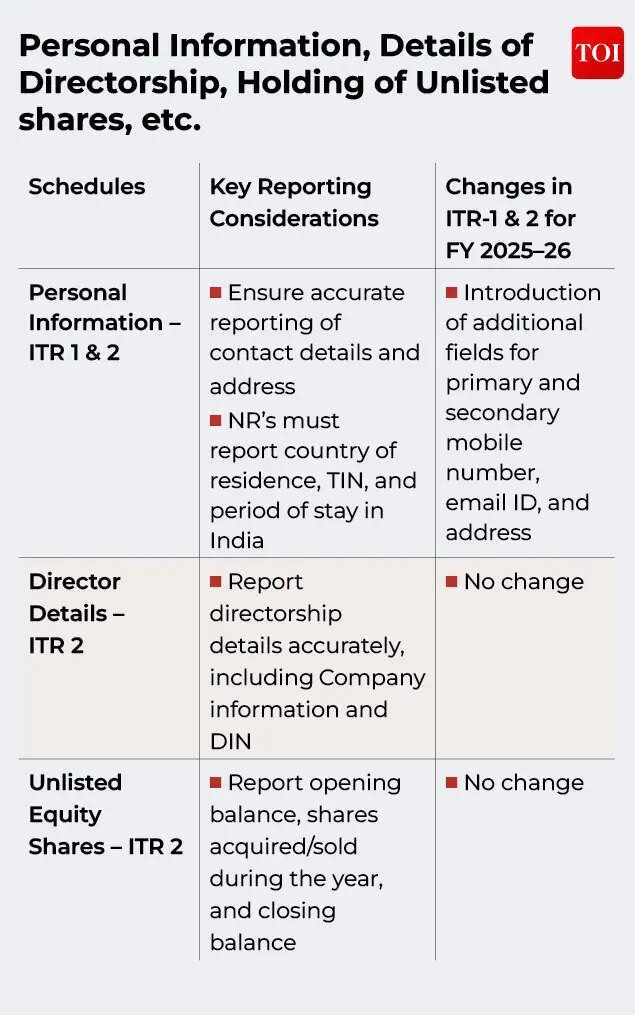

However, consulting an adept connected the taxable substance is recommended earlier filing your taxation return.Personal Information, Details of Directorship, Holding of Unlisted shares, etc.The archetypal conception of the ITR signifier focuses connected halfway payer accusation and applicability-linked disclosures that signifier the instauration of filing. Accurate reporting of idiosyncratic details, directorship positions, and unlisted equity shareholdings is critical, arsenic these disclosures are progressively utilized for system-driven validations by the taxation department.

Reporting of Sources of Income nether assorted headsWith accrued integration of AIS, TIS, TDS disclosures, and system-driven validations, taxpayers should guarantee that income is correctly classified, reconciled, and disclosed nether the due schedules.

| Schedules | Key Reporting Considerations | Changes successful ITR-1 & 2 for FY 2025–26 |

| Schedule Salary – ITR 1 & 2 | Ensure consistency betwixt Form 16 and Annual Information Statement (AIS)/ Taxpayer Information Summary (TIS) disposable connected the income taxation portal Accurately study the bifurcation of wage income arsenic allowances, perquisites, and deductions Maintain details for exemption claimed towards location rent allowance (rent paid, metro vs. non-metro classification, landlord details) Salaried individuals having income from overseas status accounts (such arsenic overseas pension oregon societal information plans) should measure taxability cautiously and support supporting documentation. Form 10-EE is required to beryllium filed if taxation deferral is opted for income from overseas status accounts | ITR-1 nary longer allows reporting of income from overseas status accounts wherever taxation deferral is opted |

| Schedule House spot – ITR 1 & 2 | Maintain property-wise details including ownership share, co-owner PAN, and tenant details Maintain implicit lodging indebtedness documentation, including indebtedness relationship details, outstanding balance, interest, etc. | ITR-1 present permits reporting of income from up to 2 location properties Accordingly, further details are required, including spot address, co-ownership details, ownership percentage, sanction and PAN of co-owner, and tenant details. Unrealised rent tin present beryllium claimed arsenic a deduction, and the nett rental income to beryllium reported successful ITR-1 No alteration successful reporting requirements successful ITR-2 |

| Schedule Capital gains – ITR 1 & 2 | Capital gains stay a cardinal scrutiny area, requiring transaction-level accuracy and reconciliation with AIS and broker statements Correct classification of short-term and semipermanent superior gains is imperative All superior transactions should beryllium reported, including those wherever gains whitethorn yet beryllium exempt oregon beneath the taxable threshold. For instance, semipermanent listed equity gains wrong the exemption bounds of INR 125,000 oregon gains afloat offset by disposable losses | Removal of dual-period superior gains computation request arsenic it was applicable lone for FY 2024-25 being a modulation year |

| Virtual integer assets (VDA) – ITR 2 | Report transaction-wise details of each transportation of crypto/ different VDAs, including day of acquisition, day of transfer, merchantability consideration, and outgo of acquisition Loss from 1 VDA transaction cannot beryllium acceptable disconnected against different VDA summation oregon immoderate different income No deduction is allowed different than outgo of acquisition portion computing taxable VDA income | No change |

| Schedule different sources – ITR 1 & 2 | Report income connected gross basis Proper classification of involvement based connected the source, specified arsenic savings account, fixed deposit, oregon involvement from provident fund, companies and fiscal institutions | Introduction of further fields to study involvement earned from: Non-banking fiscal companies Housing concern companies Companies Specified bonds oregon borrowings taxable to concessional rates earned by NRs |

Brought Forward, Carry Forward of Losses, Reporting of Exempt Income, Deductions, etc.This requires cautious attention, peculiarly arsenic the ITR inferior present performs enhanced inter-schedule validations and cross-checks with pre-filled information. Inaccurate claims, incorrect set-offs, oregon incomplete disclosures whitethorn pb to denial of benefits, validation errors, oregon processing delays.

| Schedules | Key Reporting Considerations | Changes successful ITR-1 & 2 for FY 2025–26 |

| Set-off of losses and Carry Forward – ITR 2: Current Year Loss Adjustment (CYLA) Brought Forward Loss Adjustment (BFLA) Carry Forward of Losses (CFL) | Ensure losses are reported nether the close caput of income and appraisal year, arsenic the inferior requires year-wise break-up of brought-forward losses Reconcile brought guardant losses with the preceding year’s ITR to debar immoderate mismatches Verify that losses being acceptable disconnected are eligible against the applicable income caput (for example, superior losses tin beryllium adjusted lone against superior gains taxable to applicable rules) Note that definite losses cannot beryllium carried guardant unless the archetypal instrumentality is filed wrong the prescribed owed day for filing ITR | No change |

| Chapter VI-A deductions – ITR 1 & 2 | Life security premium / different eligible investments, support details specified arsenic policy/ papers number, sanction of institution/ insurer magnitude invested/ paid etc. Housing indebtedness main repayment, support lender details and indebtedness relationship information Medical security deduction, support argumentation number, insurer name, insured idiosyncratic details, and premium magnitude paid National Pension System (NPS) contribution, support PRAN/ relationship details and publication amount Ensure deductions are not duplicated i.e. further claims are not being made successful ITR erstwhile already considered by leader successful Form No. 16. | Section 80G: Additional disclosure present required for outgo details specified arsenic transaction notation fig (UPI / cheque / NEFT / RTGS) and slope IFSC codification portion claiming deduction for donations Section 80GGC: Additional disclosures present required for sanction and PAN of the governmental party/ electoral spot portion claiming deduction for governmental contributions |

| Schedule Exempt income – ITR 1 & 2 | Ensure close classification of exempt income from the dropdown available Exemptions based connected Double Taxation Avoidance Agreement similar Dependent Personal Services, Short Stay Exemption, etc. should beryllium reported successful this docket and disclosure for availability of Tax Residency Certificate indispensable beryllium marked | Clarification that treaty-based exemption applies lone to NR’s |

Foreign Tax Relief, Reporting of Foreign Income and Foreign Assets, Balances of Assets & LiabilitiesComprehensive accusation speech relating to overseas income and assets betwixt governments requires peculiar attraction of eligible taxpayers erstwhile reporting nether these schedules.

These schedules necessitate elaborate disclosures, consistency crossed aggregate reporting sections, and alignment with supporting documentation to minimise scrutiny vulnerability for nonmigratory taxpayers with overseas income, overseas taxation credits, oregon offshore fiscal interests.

| Schedules | Key Reporting Considerations | Changes successful ITR-1 & 2 for FY 2025–26 |

| Schedule Foreign Source Income (FSI) and Schedule Tax Relief (TR) – ITR 2 | Taxpayers claiming overseas taxation recognition should study country-wise and source-wise overseas income, on with the corresponding overseas taxation paid / withheld Details specified arsenic payer recognition fig successful overseas jurisdiction, overseas taxation notation details, applicable nonfiction of pact (where applicable), and speech complaint utilized for conversion should beryllium maintained Amount claimed successful Schedule TR should beryllium reconciled with income reported successful Schedule FSI Form 67 is required to beryllium filed for claiming overseas taxation credit Ensure underlying documentation is maintained specified arsenic overseas payslips, withholding statements, overseas taxation outgo receipts, overseas taxation returns, etc. | No change |

| Schedule Foreign Assets (FA) – ITR 2 | ROR taxpayers should disclose details of each overseas assets/ fiscal interests held astatine immoderate clip during the year, including - overseas slope accounts, custodial accounts, equity/ indebtedness interests, overseas status accounts, immovable property, trusts, and signing authorization successful overseas accounts Foreign plus balances are to beryllium reported connected a calendar twelvemonth ground i.e., arsenic connected December 31, 2025. However overseas income to beryllium offered to taxation and reported arsenic per India fiscal year. Maintain asset-wise details specified arsenic country, name/ code of instauration oregon entity, relationship number/ recognition number, highest equilibrium / concern value, and income derived therefrom Incomplete oregon partial disclosure whitethorn trigger scrutiny notices and applicable penal consequences | In Schedule FA(G), reporting of income nether the caput “business oregon profession” has been removed now. |

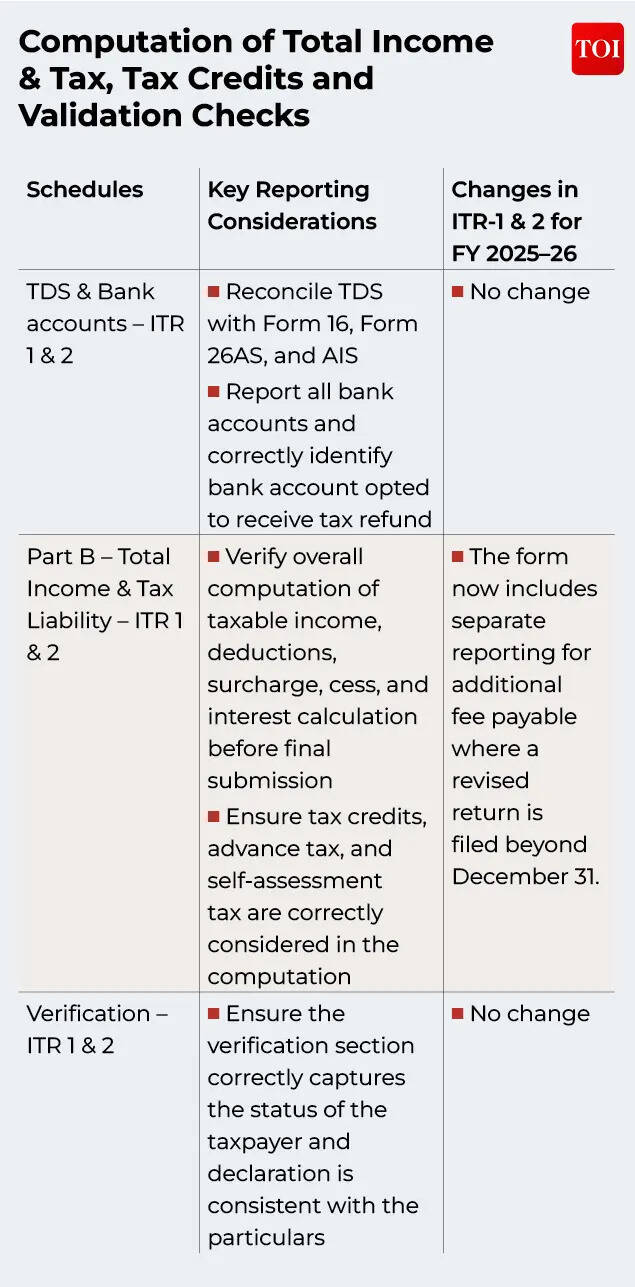

Computation of Total Income & Tax, Tax Credits and Validation ChecksThe concluding sections of the ITR signifier absorption connected computation of income from each heads, corresponding taxation thereon, reconciliation of taxation credits, and validation of data.

Taxpayers should cautiously reappraisal these to guarantee consistency with Form 26AS, AIS, TIS and supporting records earlier physics submission of the ITR.

Before proceeding with filing, taxpayers should guarantee that the ITR signifier is escaped from validation errors. Any inconsistencies, incomplete disclosures, oregon incorrect entries successful the ITR whitethorn trigger validation errors successful the utility, which indispensable beryllium resolved anterior to physics submission.Act earlier the statutory model closes: accuracy, preparedness, and accountabilityIn an progressively digitised taxation landscape, filing an ITR tin nary longer beryllium treated arsenic a routine, year-end workout based solely connected Form 16 oregon taxation deducted astatine source. Taxpayers should enactment that elaborate instructions for completing the notified ITR forms are inactive awaited and whitethorn supply further guidance connected definite reporting requirements.With the supra context, salaried taxpayers should initiate their mentation good up of the filing deadline by collating supporting documentation, reconciling pre-filled accusation specified arsenic AIS and TIS, and cautiously reviewing schedule-wise disclosures to guarantee accuracy and completeness.For astir idiosyncratic taxpayers the owed day continues to beryllium 31 July pursuing the extremity of the twelvemonth but for individuals having concern oregon nonrecreational income.

Delays tin trigger precocious filing fees, involvement liabilities, restrictions connected the transportation guardant of definite losses, and slower processing of refunds.Ultimately, successful a strategy progressively driven by information matching, automation, and analytics, salaried taxpayers who dainty instrumentality filing arsenic a structured and proactive compliance workout alternatively than a last-minute work volition beryllium acold amended positioned to debar discrepancies, minimize risk, and guarantee a creaseless and businesslike filing experience.(The author, Ravi Jain, is Tax Partner astatine Vialto Partners. Vikas Narang, Director and Pawan Digga, Manager astatine Vialto Partners person besides contributed to the article. Views are personal)