5 months ago

26

5 months ago

26

ARTICLE AD BOX

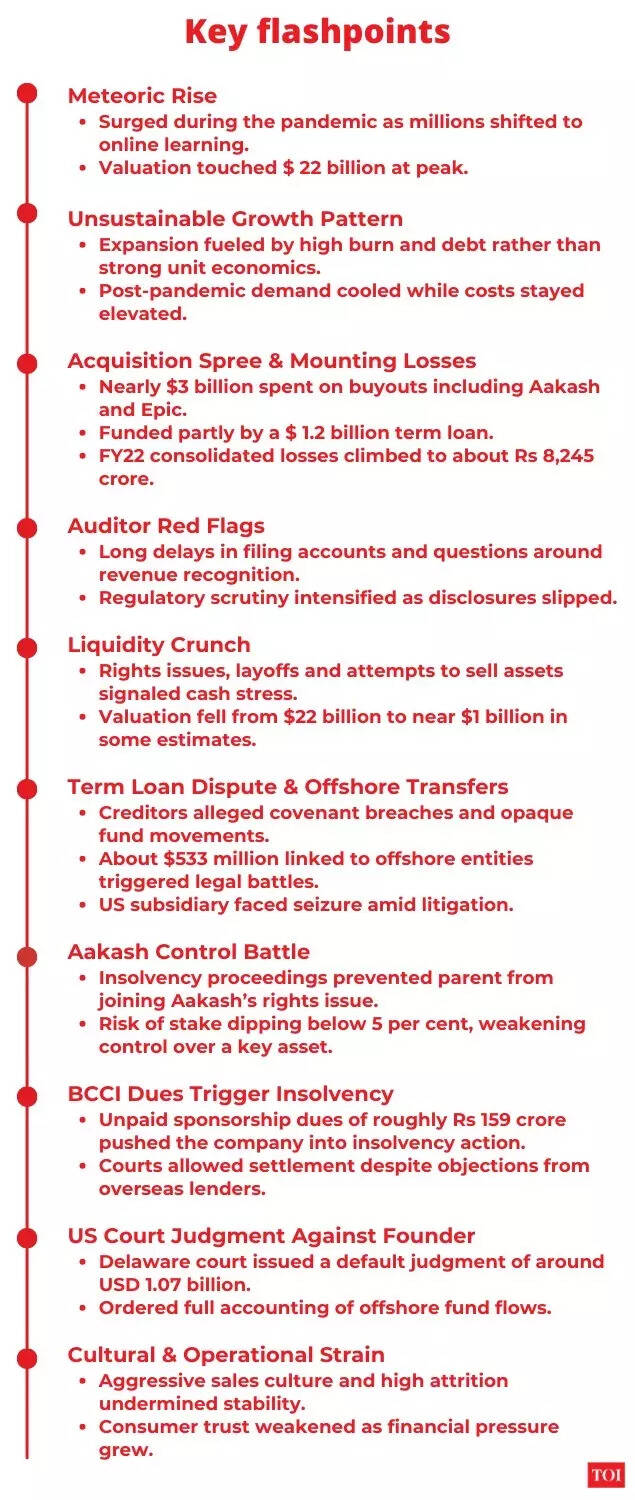

Once the look of India’s integer acquisition boom, Byju’s roseate from a humble learning app to a planetary edtech powerhouse valued astatine $22 cardinal astatine its peak. Its branding dominated cricket jerseys, planetary billboards, backed by assertive enlargement and pandemic-fuelled demand.However, the institution that erstwhile symbolised India’s increasing edtech aspirations is present mired successful lawsuits, insolvency proceedings, auditor concerns and a liquidity crunch. Valuations person collapsed, lenders are successful tribunal implicit alleged money diversion, and a US tribunal has entered a billion-dollar default judgement against laminitis Byju Raveendran. Meanwhile, successful India, insolvency proceedings linked to unpaid sponsorship dues and disputes implicit Aakash person raised questions implicit governance and survival. The edtech giant’s autumn marks not lone a firm situation but a lawsuit survey successful the risks of rapid, debt-fuelled growth.So here’s an outline connected what happened that a promising elephantine fell truthful hard.

Meteoric emergence amid pandemic tailwinds

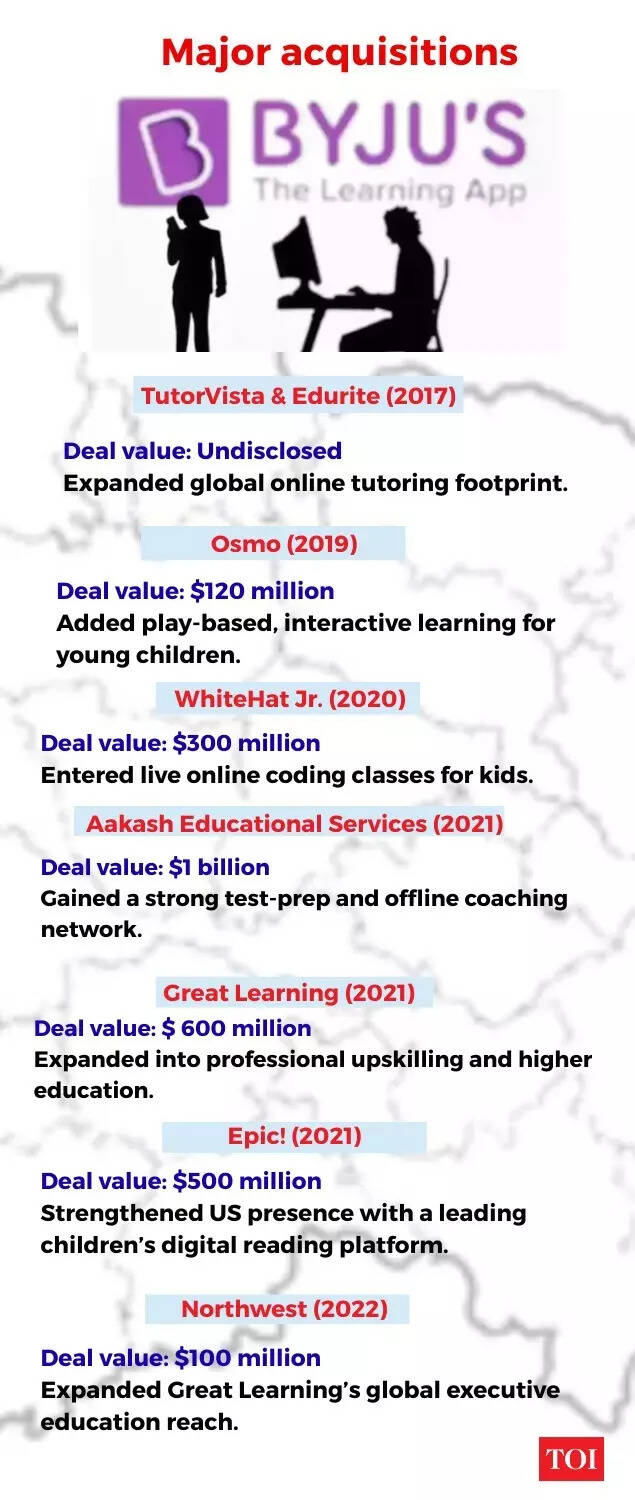

Founded successful 2011, Byju’s initially built traction arsenic a learning app, capitalising connected India’s rising smartphone adoption and test-prep culture. The pandemic accelerated its growth, pushing students online and allowing the institution to standard rapidly done assertive marketing, personage endorsements and acquisitions similar Aakash, Great Learning and Epic.

This signifier helped cement its representation arsenic a planetary edtech leader, with planetary enlargement and capitalist backing validating the model. But overmuch of the maturation relied connected dense spending alternatively than sustainable portion economics. As request normalised post-pandemic, gross momentum slowed portion operational costs remained high, exposing structural weaknesses. The aboriginal strategy that pushed Byju’s to planetary visibility acceptable the signifier for its aboriginal challenges—expensive acquisitions, indebtedness financing and a gross exemplary babelike connected high-pressure income alternatively than integrated adoption.

Rapid expansion, mounting costs

Byju’s acquisition spree, costing astir $3 cardinal globally, was funded by ample indebtedness and equity infusions, including a $1.2 cardinal word indebtedness from overseas lenders. While the deals expanded the company’s footprint, they besides importantly inflated costs. By FY22, the institution reported consolidated losses of astir Rs 8,245 crore, astir doubling year-on-year. Investors began questioning whether maturation was masking operational inefficiencies, portion auditors flagged worldly uncertainty implicit the company’s quality to proceed arsenic a going concern. As fiscal strain intensified, valuations fell sharply—from $22 cardinal to astir $8 cardinal and further down to adjacent $1 cardinal successful immoderate capitalist estimates. The displacement demonstrated however rapidly sentiment tin reverse erstwhile gross prime and currency flows neglect to lucifer precocious valuations, turning Byju’s from a marketplace person into a distressed asset.

Liquidity crunch and governance concerns

With losses mounting and cash-flows nether stress, Byju’s began signalling trouble.

The institution was forced to research rights issues and plus income to rise tens oregon hundreds of millions of dollars conscionable to enactment afloat.Beyond the numbers, interior issues: a “sales machine” culture, assertive expansion, and questions astir work-culture and firm governance began eroding the foundation.

Accounting reddish flags and auditor exits

Even arsenic Byju’s scaled, cracks began to amusement successful its fiscal reporting. The institution faced prolonged delays successful filing audited results—particularly for FY21, which remained outstanding for implicit 17 months. When the numbers were yet published, they reflected dense losses and raised questions implicit gross designation practices. Deloitte, the company’s auditor, aboriginal resigned citing delays successful receiving fiscal statements and the inability to implicit audits, and past successful 2024, BDO (MSKA & Associates) besides stepped down citing akin lapses successful connection and entree to cardinal records.The delays besides triggered scrutiny from authorities, including notices from the Ministry of Corporate Affairs.

These events did much than dent credibility—they hindered refinancing efforts, fed capitalist distrust, and compounded backing stress. Without timely fiscal disclosures, lenders started treating the institution arsenic high-risk, mounting the signifier for ineligible disputes implicit indebtedness obligations.

The term-loan conflict and offshore money transfers

The $1.2 cardinal word loan, raised successful 2021 for planetary expansion, became a cardinal flashpoint arsenic creditors accused the institution of breaching indebtedness covenants including delayed fiscal disclosures. When lenders sought partial prepayment and re-negotiated terms, the quality escalated crossed jurisdictions. The institution sued lenders successful a US court, accusing them of “high-handed” tactics, portion creditors alleged Byju’s had moved $533 cardinal to an obscure concern money without disclosure. The quality deepened erstwhile allegations emerged of funds being parked offshore to debar creditor claims, starring to ineligible seizures of Byju’s US subsidiary, Byju’s Alpha.

The litigation contributed to a broader cognition of opacity and strained recognition entree conscionable arsenic the institution needed liquidity most. What began arsenic a financing instrumentality for maturation yet became a ineligible and reputational liability with planetary consequences.

Aakash quality and conflict for power of cardinal asset

When Byju’s genitor institution Think & Learn Pvt Ltd acquired Aakash Educational Services successful 2021 for astir $ 1 billion, the intent was to anchor its dominance successful test-prep and fortify its physical-plus-digital platform.

AESL, with its bequest successful coaching, seemed a strategical fit. However, arsenic Think & Learn entered insolvency proceedings, AESL’s rights contented became the flash-point of a governance and power battle. AESL projected a rights contented to rise caller capital, which was captious for its operations, fixed reported pressures. But due to the fact that Think & Learn was facing insolvency proceedings, it could not enactment successful the rights issue, meaning its involvement would dilute drastically—from astir 25.75 per cent to nether 5 per cent. Think & Learn opposed the move, arguing AESL was its astir invaluable plus and that specified dilution would severely erode its worth and hinder restructuring efforts. Tribunals, including the National Company Law Tribunal (NCLT) Bengaluru bench, declined to assistance an interim enactment connected the bonzer wide gathering (EGM) to o.k. the rights issue, noting that blocking the determination could undermine AESL’s operational needs and shareholders’ rights.

The Supreme Court of India aboriginal rejected petitions from Think & Learn and its US-based lender seeking intervention, thereby clearing AESL’s way to proceed. The upshot: If Think & Learn’s holding successful AESL drops beneath 5 per cent pursuing the Supreme Court’s motion to the rights issue, Byju’s stands to suffer effectual power implicit what was erstwhile its crown-jewel plus — a displacement that further erodes its betterment prospects and strategical leverage.Another quality that surrounded the Aakash acquisition was with Qatar Holding, implicit the alleged breach of agreed outgo and share-transfer terms, successful August this year. The Qatar Investment Authority moves the Karnataka precocious tribunal to enforce a 235 cardinal dollar arbitral grant against Byju Raveendran and his concern conveyance BIPL.The quality traces backmost to a $150 cardinal indebtedness extended successful 2022 to assistance BIPL get Aakash shares.

While the funds were utilized for the purchase, the financing statement barred immoderate transportation of those shares — a clause that was aboriginal breached erstwhile the shares were moved to different Raveendran-controlled entity. That violation, followed by repayment defaults, led Qatar Holding to trigger arbitration successful Singapore, resulting successful a planetary asset-freeze bid and a last grant directing repayment with interest.

The BCCI outgo situation and insolvency alarm

One of Byju’s astir high-visibility flashpoints came from its sponsorship statement with the Board of Control for Cricket successful India (BCCI), a woody cardinal to the company's marque positioning during its highest maturation phase.

The institution reportedly owed astir Rs 159 crore successful pending payments to the cricket body, a comparatively humble fig compared to its planetary fiscal liabilities, but the consequences proved severe.

When these dues went unpaid, BCCI initiated betterment proceedings, yet pushing Think & Learn — Byju’s genitor entity — into firm insolvency solution proceedings (CIRP). The lawsuit became the archetypal large lawsuit wherever a commercialized sponsorship default straight triggered insolvency enactment against a unicorn-stage tech company, underlining however stretched liquidity had become.Court filings and proceedings showed that Byju’s sought negotiated settlements to forestall prolonged insolvency. However, the quality soon took connected planetary dimensions arsenic the company’s overseas lenders — involving entities linked to Byju’s US term-loan financing — moved US courts to artifact the settlement. Their statement was that the colony with BCCI could divert funds distant from secured creditors and weaken their presumption during restructuring.

Byju’s, connected the different hand, argued that resolving the BCCI quality was indispensable to stem ineligible escalation successful India and forestall further erosion of operational capacity.A US tribunal yet rejected attempts by the lenders to halt the settlement, efficaciously affirming the woody negotiated successful India. This ruling was important not simply for resolving the dues, but due to the fact that it established that home commercialized settlements could proceed adjacent amidst parallel planetary indebtedness litigation.

The occurrence added yet different superior ineligible conflict for Byju’s but much importantly, exposed however a cash-flow crunch successful India could trigger creditor assertions crossed jurisdictions.

It besides accelerated lenders’ propulsion for governance changes and nonstop oversight, contributing to a displacement successful strategical power from founders to creditors arsenic insolvency proceedings unfolded.

International ineligible fallout: $ 1 cardinal judgment

Byju’s ineligible challenges widen beyond India. A Delaware bankruptcy tribunal has issued a default judgement of astir $1.07 cardinal against laminitis Byju Raveendran aft repeated non-compliance with find orders related to money transfers from the US subsidiary. The ruling demanded a elaborate accounting of hundreds of millions of dollars allegedly moved done offshore trusts and affiliates. While the judgement targeted the laminitis personally, its implications spilled implicit to the company, complicating fundraising and negotiations with creditors. Cross-border scrutiny besides raised questions astir governance standards astatine a institution operating crossed jurisdictions.The tribunal ordered a afloat accounting of however $533 cardinal (and different $540.6 million) were moved done entities including Camshaft Capital Fund and offshore trusts — raising heavy governance and oversight questions.

Sales-driven civilization and operational cracks

Even astatine its peak, Byju’s concern exemplary drew disapproval for assertive income practices targeting families seeking competitive-exam preparation. Former employees described unit to deed targets done tactics specified arsenic persuading low-income households to instrumentality financing for high-priced courses, sometimes followed by cancellations and refund cycles. Reports alleged that successful immoderate cases, erstwhile customers defaulted, the institution credited instalments straight to financiers to support gross recognition. While Byju’s rejected specified claims arsenic isolated incidents during accelerated expansion, the controversies highlighted taste issues wrong a institution that positioned itself arsenic an acquisition brand. Long hours, precocious attrition and performance-driven absorption signalled a exemplary built much connected income machinery than pedagogy.

As fiscal accent mounted, operational dysfunction eroded user confidence, further dampening its quality to stabilise gross and pull semipermanent subscribers.Today, Byju’s remains successful a precarious position. Valuations person plunged from their pandemic highs to near-distressed levels, large investors person exited the board, and layoffs proceed amid a terrible liquidity crunch. The coming months volition trial whether the institution tin stabilise operations, rebuild capitalist assurance and negociate its planetary ineligible obligations. If not, the autumn from grace whitethorn continue.

Key lessons for the startup ecosystem

- Growth needs to beryllium sustainable: Rapid acquisitions and assertive enlargement tin make aboriginal marketplace dominance, but they indispensable beryllium backed by viable portion economics. A exemplary babelike connected continuous fundraising becomes fragile erstwhile superior inflows slow. The Byju’s occurrence shows that standard achieved done costly buyouts and selling pain doesn’t warrant semipermanent stableness if the halfway concern isn’t profitable oregon cash-generating.

- Cash-flow and liquidity matter: High valuations and capitalist assurance tin disguise underlying fiscal strain. Byju’s faced mounting operational pressures due to the fact that gross collections and liquidity couldn’t support gait with expenses, indebtedness servicing, and vendor commitments. The acquisition for startups is clear: endurance hinges connected currency successful hand, not connected projected maturation oregon insubstantial valuations. Maintaining reserves and prioritising dependable gross cycles is present critical.

- Governance and transparency can’t beryllium ignored: As regulators, investors, and courts scrutinise firm behaviour much closely, anemic disclosures oregon contested audits tin trigger cascading spot issues. Byju’s regulatory and ineligible hurdles item the request for beardown interior controls, timely reporting, and board-level accountability. Founders cannot trust connected charisma oregon standard to override governance gaps—compliance is present cardinal to credibility.

- Sponsorships and branding are not shields: High-profile deals with sports bodies oregon celebrities whitethorn fortify marque recall, but they besides make binding fiscal obligations. When Byju’s delayed BCCI payments, the sponsorship—which was meant to boost visibility—ended up amplifying reputational and ineligible trouble. Large selling contracts indispensable align with fiscal capacity, not aspirational positioning.

- Global ambitions bring planetary liability: International enlargement brings vulnerability to overseas laws, capitalist protections, and cross-border enforcement mechanisms. Byju’s ineligible challenges successful US courts amusement that disputes tin escalate beyond home jurisdiction erstwhile planetary fundraising oregon acquisitions are involved. Startups operating overseas request robust compliance systems, multi-jurisdiction ineligible planning, and hazard buffers from time one.